Central bankers like Federal Reserve Chair Jerome Powell in the United States and European Central Bank President Christine Lagarde are powerful yet unelected. Their key job is to set domestic interest rates. Many governments also task their central banks with ensuring stability in the financial sector. Over the last 35 years, most countries have passed laws that grant central bankers pursuing these tasks legal insulation from elected officials. This means governments willingly relinquished some democratic control, and delegated monetary policy to independent central banks.

The institutional mechanisms for independence include fixed and lengthy terms for central bank governors, legal protections against arbitrary dismissal, clear mandates prioritizing price stability, and prohibitions against central bank lending to the government. These features have been codified in global indices of legal central bank independence.

The trend towards greater legal independence for central banks has been truly a global phenomenon. Central banks gained legal independence in countries as diverse as Venezuela, Russia, and Belarus, on the one hand, and the United Kingdom, Japan, Chile and the Czech Republic, on the other. In fact, central bank independence has been one of the true global norms of good economic governance. International financial institutions have long promoted central bank independence as a best practice. And the rewards for countries have been clear: foreign investment flourished and the economies of countries around the world grew.

The importance of sound money

Most people dislike inflation. And rising prices frequently undermine economies, whether it’s post-covid inflation in the U.S. and elsewhere, or examples from post-communist Eastern Europe and countries in Latin America. The job of the independent central bank is to provide an important public good: stable prices. Central bankers are usually more concerned about inflation than politicians, in fact. Theoretically, central bank independence should keep inflation in check by tying governments’ hands from using monetary policy for political ends.

The alternative scenario is leaving it up to governments to control monetary policy. But that gives political leaders strong incentives to use monetary policy to spur economic growth for electoral benefit. An added challenge is that financial markets, businesses, and households will anticipate such incentives and expect higher inflation when they make decisions about investments, purchases, and myriad other economic and financial matters. The results of this strategic interaction will be inflation, undermining economic growth.

Empirical research has shown that countries benefit from having a more independent central bank. These countries enjoy lower inflation and lower rates of monetary growth – and also attract more foreign direct investment and have better credit ratings. These benefits appear to come without a decrease in economic growth. Central bankers like Janet Yellen, the former U.S. Federal Reserve chair, proclaim that “central bank independence promotes better economic performance.”

Political influence of central banks

Yet, the touted independence is based on legal protections that in practice can be quite pliable. This inevitably leaves central banks steeped in politics. Publicly or behind closed doors, governments continue to push for lower interest rates.

This is not surprising, and is not even undesirable. While modern central bankers have a preference for low inflation – which works well to keep prices stable – those preferences may also put too little value on employment levels and can favor the interests of the financial sector or the political right and the rich. So, contestation around how central banks work within laws giving them independence from day-to-day politics is a sign of healthy debate about accountability: how to interpret legal mandates, how to look at economic data, and how to weigh future risks.

Yet that contestation can easily veer into overt politicization in several ways. Threats to fire central bankers despite legal limits around dismissal is one example. Other examples of politicization include actually firing central bankers in countries like Turkey or Argentina – or explicit threats to change the laws granting central banks independence, as was the case in Hungary, Argentina, and Venezuela. These situations point to a sustained, public challenge to the legitimacy of central banks. For the political leaders involved, the ultimate goal was to re-exert government control over monetary policy.

In monetary policy, the rule of law matters

Research shows that legally independent central banks have their clearest effect on inflation in countries with strong rule of law traditions. Very directly, this works because in such countries any change to legislation – in this case central bank laws – is delayed by a process of building a new consensus in which different political and societal groups weigh in. Arguing the case in the media or litigating it in the courts helps ensure the issues remain transparent.

Effective rule of law thus presumes the existence of strong constraints on executive power. It also presumes the presence of vibrant civic organizations and interest groups, as well as a free media and independent courts. Only under such conditions will laws afford central bankers autonomy to focus on the economic data and give the broader public a reason to lower inflation expectations. Only then can laws governing central banks actually help deliver the public good of stable money. For example, in 2012, Jens Weidmann, the president of the Deutsche Bundesbank at the time, wrote:

Delivering on its primary goal to maintain price stability is the prerequisite for safeguarding the most precious resource a central bank can command: credibility. In monetary policy, as in life, you will be tomorrow what you do today.

There is thus a fine line between overt pressure that undermines the independence of the central bank and a healthy democratic debate about how central banks can do their legislated job.

How independent is the U.S. Federal reserve?

Based on the 1913 Federal Reserve Act and its 1935 overhaul, the Fed is only moderately independent, many scholars believe. While the Fed is self-financed and thus highly independent in that regard, the central bank chair and vice chairs are appointed only for 4 years. And U.S. law does not explicitly protect the Fed chair from dismissal, which decreases the independence of the U.S. central bank. (That said, the chair also serves as a member of the Fed’s Board of Governors, whose seven members are appointed for a remarkably long, 14-year term and can only be removed for cause).

The Federal Reserve Act specifies both inflation and unemployment as policy mandates, rather than the main goal of price stability. This point leaves room for political influence, muddling accountability, and complicating the quest for low and stable prices in the United States. In practice, ever since the Paul Volcker era of the 1980s, financial markets and the public perceive the U.S. Federal Reserve to be significantly more independent than a strict interpretation of the law might suggest. A U.S.president has never fired the Fed chair. And Fed independence has generally had bipartisan support from Congress – and, importantly, enjoys strong backing within the influential U.S. financial sector.

Still, support from Congress or the White House is not guaranteed. While the U.S. Federal Reserve has a clear legal responsibility to report to the legislative branch, Congress has periodically imposed greater transparency requirements. Even after amending the Federal Reserve Act in the 1970s to require audits of the Fed, lawmakers in recent years continue to propose additional “audit” the Fed bills, seeking to require the U.S. Government Accountability Office to scrutinize the Fed’s monetary policy committee decisions. In another example, Republican presidential nominee Mitt Romney suggested in 2012 that the Fed should be audited. Romney also said that he would not plan to reappoint Fed Chair Ben Bernanke.

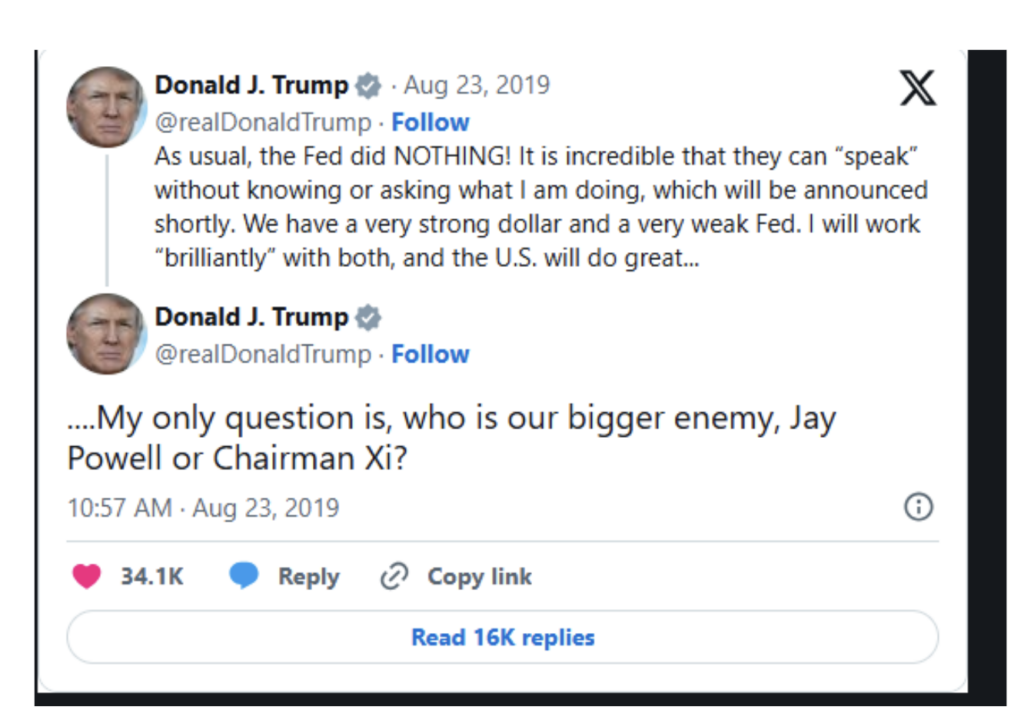

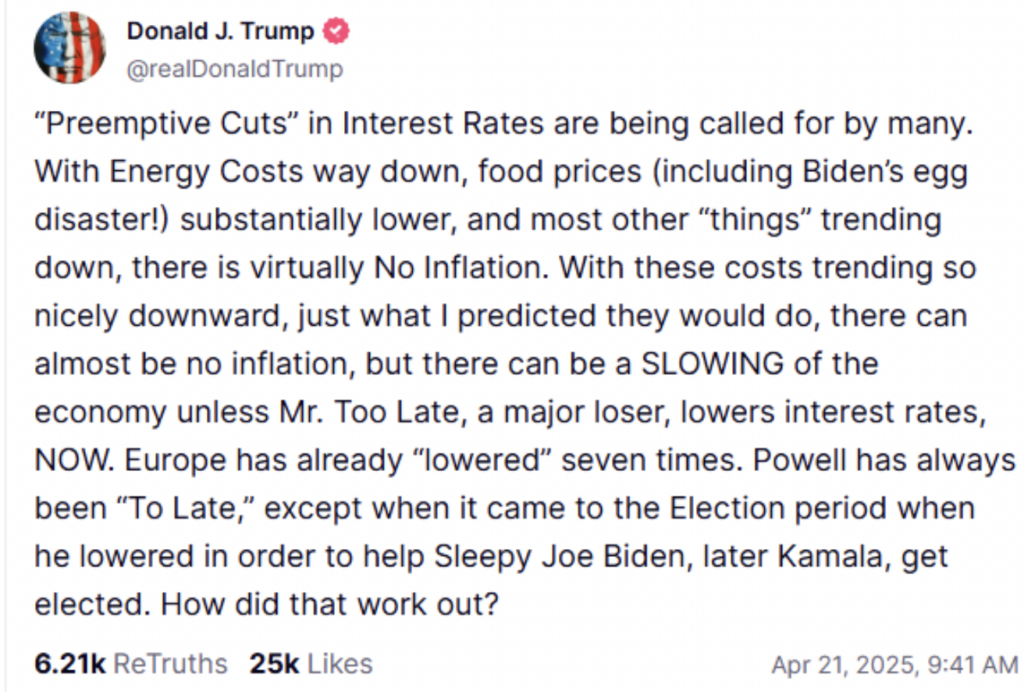

Trump has frequently attacked the Fed

In his first term in the White House, Donald Trump consistently bullied the Fed to lower interest rates. Trump often mused about firing firing Powell – his own appointee to the position of Fed chair.

Those verbal scoldings did have an effect on how Americans view inflation, as well as how elites viewed Fed independence. In Trump’s second term in office, however, his attacks on the Fed and Powell take on new meaning. This is because these attacks are now coupled with a significantly worsening outlook for the rule of law in the U.S.

A year ago, many economists praised the Fed’s efforts to deliver a soft landing for the U.S. economy. But the Federal Reserve now stands to lose all credibility that it is looking at inflation and unemployment data with an impartial eye. The consequences for the U.S. economy are bad: higher inflation expectations, followed by the self-fulfilling prophecy of inflation, as well as significantly higher employment costs when it comes to tackling the inflation problem.

The rule of law can boost the Fed’s credibility

Central bank independence is a clear example of institutional design delegating a part of governments’ job – in order to enhance policy credibility. This comes at a cost for democratic control over the economy, and debate about how central banks should function within the law are welcome. However, as with other formal institutions, the rule of law ultimately provides the institutional scaffolding that allows central bank laws to function as legislated – and lets them do their job to stabilize the economy.

Cristina Bodea is a professor of political science at Michigan State University. She studies central banks, exchange rates and gender and political economy.

Raymond Hicks is associate research scholar in the Department of History at Columbia University. He studies central banks, trade policy and big data.